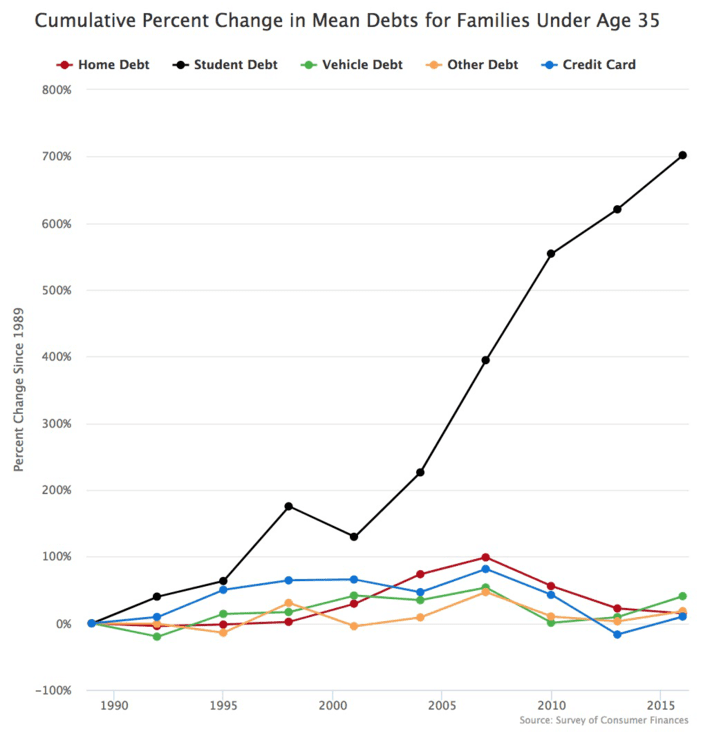

For families under age 35, growth of student debt outstrips by far the growth of any other debt source, including mortgage and credit card debt (source).by Gaius PubliusIn America today, 44 million people collectively carry $1.4 trillion in student debt. That giant pile of financial obligations isn’t just a burden on individual borrowers, but on the nation’s entire economy.In the world of parasites, the job of the parasite is to benefit from the harm it does to the host, but not to kill the host, at least not until the parasite is done with it:

{kind=link}

In biology, parasitism is a relationship between species, where one organism, the parasite, lives on or in another organism, the host, causing it some harm, and is adapted structurally to this way of life. The entomologist E. O. Wilson has characterised parasites as "predators that eat prey in units of less than one".... Unlike predators, parasites, with the exception of parasitoids [examples: wasps that lay eggs in paralyzed spiders, or the beast in Alien], typically do not kill their host, are generally much smaller than their host, and often live in or on their host for an extended period. Parasitism is a type of consumer-resource interaction. [Footnotes removed]

Parasites are not the same as predators. Predators kill, eat, and move on. Parasites disable, then live off the energy system of the disabled host for as long as they can keep the host alive.Viruses are a form of parasite. So are credit card companies.Loan Companies as ParasitesThe parasite first disables the host's ability to reject the parasite, then derives its own energy (that which sustains it) by robbing the host's energy system. It attempts to do this for as long as possible. Loan companies whose "business plan" — survival strategy — is to prolong the loan, and at the maximum sustainable rate, are by definition parasites.But there is a scale of parasitism among loan companies. The least parasitic are mortgage companies, in that mortgages typically don't destroy incomes; they just feed off them. When the host goes into bankruptcy (usually for other reasons, such as illness, divorce or job change), the host (the home-owner) is abandoned, but mortgage company parasites don't typically cause these bankruptcies by themselves.In addition, if a host wants to repay her debt and free herself from the parasite, she is allowed to do so, though typically, hosts usually seek a new parasite, either by necessity or because of cultural pressure. At the less gentle end of the parasitic spectrum are payday lenders and loan sharks, who actually disable the host's income capability by extracting so much money that the host almost certainly goes bankrupt, often first drawing on the resources of others and transferring those resources to the parasite as well before they do.Payday lenders thrive in an environment rich in new hosts, since so many of their former ones become useless. In contrast, most mortgaged homeowners (hosts of mortgage banks) don't go bankrupt — just some of them. Student Debt Parasites Feed on Especially Vulnerable Hosts Not far up the parasitic scale from payday lenders and loan sharks are owners and beneficiaries of student debt, i.e. the lending companies.First, as the chart above shows, there's a large and growing population of prospects in the student loan world. New hosts, it seems, are everywhere. Second, the loan amounts are extraordinarily large and extraordinarily long-lived (my emphasis throughout):

The average debt load for students who graduated in the class of 2016 was around $30,000, and the average rises every year.But some students graduate with far more debt than that, especially those who pursue graduate degrees or professional degrees. Nearly 17 percent of those who borrow for education costs will graduate owing more than $50,000, according to the recent study by the Brookings Institution. That is a much higher rate than in 2000, when five percent of new graduates owed that much money.Today, many of those who graduate with more than $50,000 in debt aren’t the students who are pursuing highly-lucrative careers, such as becoming a doctor or a lawyer, but undergraduate students and their parents. On the other hand, more people who are pursuing a professional degree are graduating with well over $100,000 in student loans.

While a student debt load of $30,000 doesn't sound large compared to mortgage debt, remember that these hosts almost never have a source of income when they incur the debt. In contrast, home loan applicants generally have to prove income prior to acquiring the debt.For high-debt graduates — greater than $50,000, greater than $100,000 — the situation is much worse. The debt burden can hobble their entire lives. I've met men and women in their thirties whose most common complaint is, "I will never get out of debt, and I will never get a job in my profession." I've met high-tech workers in high-mortgage-cost regions of the country with incomes greater than $150,000 per year, student loan repayments of nearly $2,000 per month, more than one child, and no way to break even on a month-to-month basis.All of these people are one bad-luck accident away from bankruptcy — which means good-bye to the next good job for more than a decade afterward.Student Loan Parasites Also Feed on the Economy as a WholeBut student loan parasites don't just eat and diminish the host — they eat and diminish the economy as a whole. It's an axiom in economics that aggregate debt repayment subtracts from GDP, a measure of overall economic production. In practical terms, a dollar spent repaying a debt to a lender is a dollar that doesn't buy bread, purchase services like health care, or build a factory.As a nation's private debt burden increases, private sector demand and spending falls. In the extreme, if everyone in a country decided or were forced to pay all debts at once, the overall economy would collapse. (The same would happen if everyone in an economy went on a savings spree.)This is what today's high levels of student debt are doing to our economy. Writes Eric Levitz at New York magazine:

In America today, 44 million people collectively carry $1.4 trillion in student debt. That giant pile of financial obligations isn’t just a burden on individual borrowers, but on the nation’s entire economy. The astronomical rise in the cost of college tuition — combined with the stagnation of entry-level wages for college graduates — has depressed the purchasing power of a broad, and growing, part of the labor force. Many of these workers are struggling to keep their heads above water; 11 percent of aggregate student loan debt is now more than 90 days past due, or delinquent. Others are unable to invest in a home, vehicle, or start a family (and engage in all the myriad acts of consumption that go with that).

Note that number: U.S. aggregate student debt has reached almost $1.5 trillion. A Debt Jubilee to Rejuvenate the EconomyThe obvious solution to this problem has been practiced since ancient times — a debt jubilee in which all student debts are cancelled. Keep in mind that the U/S. government owns or controls 90% of all student debt in this country:

Thus, if the government were to forgive all the student debt it owns (which makes up more than 90 percent of all outstanding student debt), and bought out all private holders of such debt, a surge in consumer demand — and thus, employment and economic growth — would ensue.According to the Levy Institute paper [here], authored by economists Scott Fullwiler, Stephanie Kelton, Catherine Ruetschlin, and Marshall Steinbaum, canceling all student debt would increase GDP by between $86 billion and $108 billion per year, over the next decade. This would add between 1.2 and 1.5 million jobs to the economy, and reduce the unemployment rate by between 0.22 and 0.36 percent.

Note that the ancient concept of "debt jubilee" doesn't necessarily apply to all debt, just unproductive debt.Economist Michael Hudson writes this about debt jubilees in Sumerian and Babylonian times:

The Bronze Age core economies coped with the debt problem simply by canceling society’s unproductive debts when they grew too large. However, the Sumerians and Babylonians only annulled consumer barley-debts; they left commercial silver-debts intact. ... This implicit distinction between productive and unproductive debt represents a third way in which Babylonian economics may be deemed more sophisticated than modern economics (in addition to the afore-mentioned focus on the destabilizing role of debts multiplying at compound interest, and the phenomenon of wealth addiction.)

Note his mention of the socially "destabilizing role of debts multiplying at compound interest," as well as the (similarly destabilizing) role of "wealth addiction." Our society is hobbled by both.Student loan debt is by definition unproductive debt — a debt owed to parasites, in other words. There is no question that cancelling it would free both hosts — the millions of graduates themselves (and those who failed to graduate), and the larger economy as well.A Moral Question and an Economic QuestionIt's certainly true that the economy as a whole would benefit from student debt cancellation. As noted, aggregate student debt is at or near $1.5 trillion, and rising.We also know that even Repubicans believe that an injection of $1.5 trillion into the economy would do a world of good. According to one Fox News defender of the recent $1.5 trillion tax cut bill, "Democrats have now become born-again deficit hawks, painting an additional $1.5 trillion added to the deficit over the next 10 years from this tax plan as causing certain harm. But they fail to take into account economic growth that would be created by tax cuts".It's true that tax cuts have a stimulus effect, but not much of one. Making the Bush tax cuts permanent, for example, had a "fiscal multiplier" (stimulus effect) of 0.26. By contrast, a one-time increase in food stamps would have a multiplier of 1.73.Quite a difference. A one-time reduction of student loan debt of $1.5 trillion would immediately pour hundreds and in some cases, thousands per month per indebted household into the productive economy — enriching not Wall Street this time, but Main Street.Everyone in the country would benefit, offering an answer to the economic question "How do we improve the lives of all Americans?"But a massive student loan cancellation would also help answer a moral question: "How do we free ourselves from the financial parasites who take money for themselves that others have earned?"Freeing a host from parasites is indeed a moral task, especially when humans are the hosts. If you doubt you have a moral response to parasites, consider the "tongue-eating louse" (pictured below).Cymothoa exigua, or the tongue-eating louse, is a parasitic crustacean of the family Cymothoidae. The parasite enters fish through the gills and then attaches itself to the fish's tongue, strangling and replacing it (source). This parasite destroys the tongue of its host, replaces the tongue so the fish thinks nothing is amiss, then slowly drains the fish as the fish feeds itself. If you owe student debt yourself, especially great amounts of it, something similar is happening to you — a large percentage of your income is going each month to people who do nothing but move money around. The only difference between you and the fish above is — you know something's amiss. Next Steps: Answering the "How?" and "What Next?" QuestionsThis answers the Why question of student debt cancellation — the moral job of freeing a host (us and our children) from parasites, the economic job of growing the productive economy so all can have better lives. I'll answer the How question — what does implementation look like? — and the What Next question in another installment.I'll also answer the What If We Don't question. Here's a hint: Extreme parasitism is not a stable system. When hosts become aware of their parasites, they fight back. GP

{kind=link}