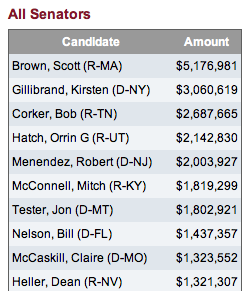

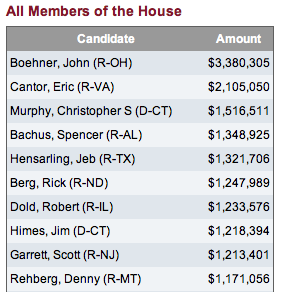

I think most Members of Congress, financed and sold out as they are to Wall Street, abhor the idea of going to war with the banksters over regulations. The finance sector spends more on bribing federal elected officials-- $663,265,994 last cycle alone-- than any other industry. And, although they give a bit more to Republicans, they give plenty to both corrupt Beltway parties. Here are the 10 biggest recipients of bankster cash last year in the Senate and in the House: Thursday Elizabeth Warren (D-MA), John McCain (R-AZ), Maria Cantwell (D-WA), and Angus King (I-ME) introduced the 21st Century Glass-Steagall Act, a modern version of the Banking Act of 1933 (Glass-Steagall) that reduces risk for bank customers and for American taxpayers in the financial system and decreases the likelihood of future financial crises. This is how much each of the senators sponsoring that bill took in bribes from the banksters last year:

{kind=link}

{kind=link}

{kind=link}

• Elizabeth Warren- 0• John McCain- 0• Maria Cantwell- $621,581• Angus King- 0

If the bill passes the Senate and House and Obama signs it, it will separate traditional banks that have savings and checking accounts and are insured by the Federal Deposit Insurance Corporation from riskier financial institutions that offer services such as investment banking, insurance, swaps dealing, and hedge fund and private equity activities. The legislation would clarify regulatory interpretations of banking law provisions that undermined the protections under the original Glass-Steagall and would make "Too Big to Fail" institutions smaller and safer, minimizing the likelihood of a government bailout. "Since core provisions of the Glass-Steagall Act were repealed in 1999, shattering the wall dividing commercial banks and investment banks, a culture of dangerous greed and excessive risk-taking has taken root in the banking world," said McCain, who joined every other Republican in the Senate to vote for repeal. "Big Wall Street institutions should be free to engage in transactions with significant risk, but not with federally insured deposits. If enacted, the 21st Century Glass-Steagall Act would not end Too-Big-to-Fail. But, it would rebuild the wall between commercial and investment banking that was in place for over 60 years, restore confidence in the system, and reduce risk for the American taxpayer." "Despite the progress we've made since 2008, the biggest banks continue to threaten the economy," said Senator Elizabeth Warren. "The four biggest banks are now 30% larger than they were just five years ago, and they have continued to engage in dangerous, high-risk practices that could once again put our economy at risk. The 21st Century Glass-Steagall Act will reestablish a wall between commercial and investment banking, make our financial system more stable and secure, and protect American families."

The original Glass-Steagall legislation was introduced in response to the financial crash of 1929 and separated depository banks from investment banks. The idea was to divide the risky activities of investment banks from the core depository functions that consumers rely upon every day. Starting in the 1980s, regulators at the Federal Reserve and the Office of the Comptroller of the Currency reinterpreted longstanding legal terms in ways that slowly broke down the wall between investment and depository banking and weakened Glass-Steagall. In 1999, after 12 attempts at repeal, Congress passed the Gramm-Leach-Bliley Act to repeal the core provisions of Glass-Steagall.

With Wall Street banksters popping open the champagne bottles, the disastrous repeal passed the House 343-86-- only 16 Republicans, 69 Democrats and, of course, independent Bernie Sanders, standing up to be counted against the obvious disaster-in-the-making. Among the House Members in 1999 who were smart (and honest) enough to vote know were this dozen, all folks who are still pretty well known today:

• Tammy Baldwin (D-WI)• Sherrod Brown (D-OH)• John Conyers (D-MI)• Barbara Lee (D-CA)• John Lewis (D-GA)• Ed Markey (D-MA)• Jerry Nadler (D-NY)• Ron Paul (R-TX)• Bernie Sanders (I-VT)• Jan Schakowsky (D-IL)• John Tierney (D-MA)• Maxine Waters (D-CA)

And among the Members of Congress too corrupt and too stupid-- the two conditions often go hand-in-hand among Members of Congress-- who backed this legislation were this two dozen, who are also still active today and still working harm to make life miserable for the ordinary American family:

• Roy Blunt (R-MO)• John Boehner (R-OH)• Richard Burr (R-NC)• Dave Camp (R-MI)• Joe Crowley (D-NY)• Jim DeMint (R-SC)• Harold Ford, Jr. (D-TN)• Steny Hoyer (D-MD)• Johnny Isakason (R-GA)• John Kasich (R-OH)• Ron Kind (D-WI)• Peter King (R-NY)• Buck McKeon (R-CA)• Rob Portman (R-OH)• Dana Rohrabacher (R-CA)• Ed Royce (R-CA)• Paul Ryan (R-WI)• Matt Salmon (R-AZ)• Mark Sanford (R-SC)• John Thune (R-SD)• Pat Toomey (R-PA)• Fred Upton (R-MI)• David Diapers Vitter (R-LA)• Anthony Weiner (D-NY)

Which list would you rather be on-- those who saw the problem and tried to stop it from happening... or those who caused the problem? More from Elizabeth Warren on the need for this legislation:

Banking should be boring. Savings accounts, checking accounts-- the things that you and I rely on every day-- should be safe from the sort of high-risk activities that broke our economy. The way our system works, the FDIC insures our traditional banks to keep your money safe. That way when you want to withdraw money from your checking account, you know the money will be there. That’s what keeps our banking system safe and dependable. But the government should NOT be insuring hedge funds, swaps dealing, and other risky investment banking services. When the same institutions that take huge risks are also the ones that control your savings account, the entire banking system is riskier. Coming out of the Great Depression, Congress passed the Glass Steagall Act to separate risky investment banking from ordinary commercial banking. And for half a century, the banking system was stable and our middle class grew stronger. As our economy grew, the memory of the regular financial crises we experienced before Glass Steagall faded away. But in the 1980s, the federal regulators started reinterpreting the laws to break down the divide between regular banking and Wall Street risk-taking, and in 1999, Congress repealed Glass Steagall altogether. Wall Street had spent 66 years and millions of dollars lobbying for repeal, and, eventually, the big banks won. Our new 21st Century Glass Steagall Act once again separates traditional banks from riskier financial services. And since banking has become much more complicated since the first bill was written in 1933, we’ve updated the law to include new activities and leave no room for regulatory interpretations that water down the rules. The bill will give a five year transition period for financial institutions to split their business practices into distinct entities-- shrinking their size, taking an important step toward ending “Too Big to Fail” once and for all, and minimizing the risk of future bailouts.